Ghana

Digital payments – even with no internet

Many people in Ghana use cash only, especially in rural areas. Thanks to a cash card with fingerprint ID, finance in Ghana is now more secure and efficient. The project is supported by KfW.

The cashier from the local bank uses e-zwich to pay government social grants to farmers in the village of Adukram.

Askia Mborta is waiting for her wages. Like the other three dozen men and women sitting with her under the shade of the trees at the edge of her village of Adukram, she works in a government job creation scheme. The cashier from the Kuwamuman Rural Bank has come down the dusty, reddish road from the district town in a small, armoured off-roader. He has brought a card reader which includes a fingerprint scanner, laying it down on a wooden bench and connecting it to a generator.

When Mborta’s turn comes, she sits down on the bench in front of the cashier. He checks over a list to see what she is due in wages. Mborta then inserts her cash card with the e-zwich logo into the device’s slot and places a finger onto the scanner. This is how the mother-of-four identifies herself as a legitimate wage earner, as her card’s chip has the prints of all ten of her fingers saved. Mborta asks for cedi (the Ghanaian currency; GHS) and a receipt from the cashier. She could also simply load her wages onto the card.

Archie Hesse would have been pleased with how the payday went in this community of mud hut homes. The Chief Executive Officer of Ghana Interbank Payment and Settlement Systems Limited (GhIPSS) sits in his office in the Ghanaian capital of Accra, five hours’ drive south of Adukram, explaining the e-zwich system with the slogan “easy banking for everyone”.

Not only cash is king

At root, banking in Ghana is by no means an easy undertaking; even less so in rural areas. There are only 140 independent rural banks around the country. Two-thirds of all districts have an institution like this with just a few branches. The process for transactions is laborious and wages are often paid with a cheque that can only be cashed at a particular bank. Cash is in great demand. But that is a problem, according to Archie Hesse, who explains that the large amount of cash in hand misses out on circulation in the financial system.

People at the central bank subsidiary GhIPSS came to the conclusion that they needed a payment system that would be fraud-proof, easy to use and workable to implement at all financial institutions. On top of that, it had to be capable of supporting illiterate users. This resulted in e-zwich being rolled out ten years ago e-zwich being rolled out ten years ago; zwich as in switch, but with a smoother pronunciation. The cardholder does not need an account – many indigent people in rural areas still do not have one. The card is the only thing necessary to pay in and take out money.

Read more under the image gallery.

New ATMs for Ghana

The Wenchi Rural Bank is located in Ghana’s inner heartland. e-zwich cardholders can withdraw money here from a total of four new automated teller machines supported by KfW.

Archie Hesse is the CEO of GhIPPS, which operates the card system. GhIPPS is an offshoot of the Bank of Ghana, the country’s central bank.

The idea sounds obvious, but nevertheless, e-zwich’s development was long-drawn-out. Customers and interested banks were lacking. Subsequently, in 2012, a package to support e-zwich was agreed between the Republic of Ghana and the Federal Republic of Germany. The implementing organisation on the German side would be KfW, which considered the project fundamentally worthy of support, though this did “demand a certain volume of transactions to be able to sustainably establish e-zwich in the market,” as project manager Jana Reinheimer from KfW Development Bank explains.

For instance, the aim was for authorities to pay wages via e-zwich. “For banks, rolling out the system is associated with costs. e-zwich’s attractiveness for them only increases when this burden of costs pays off in the long term. The higher the e-zwich transaction volume, the higher receipts from fees are for banks,” Reinheimer states. The turnover processed through the cashless system has more than trebled since 2011.

The Wenchi Rural Bank in Ghana’s inner heartland runs four of the new KfW-supported automated teller machines, at which owners of an e-zwich card can withdraw cash.

Target group is the poor rural population

KfW is making it easier for Ghanaian banks, including savings banks, to connect to e-zwich by offering them loans on favourable terms to buy hardware (cards, mobile card readers and cash points). KfW has provided seven million Euros from the funds of the German Federal Ministry for Economic Cooperation and Development (BMZ) for this purpose, with half of this sum already claimed.

Repaid amounts can then be resupplied for further hardware purchases. In this process, KfW Development Bank pays particular attention to the social impact of e-zwich. “The poor rural population is our target group,” says Reinheimer. Robert E. Austin, National Coordinator of the Ghana Social Opportunities Project (GSOP), also works to improve their plight. Poverty, Austin says, is always the consequence of a lack of access to education, hospitals and financial institutions.

The programmes run by GSOP are funded by the World Bank. In addressing the question of how to get the money to the poorest people, GSOP opted for e-zwich. The security of the biometric system gave it the edge over its competition, Austin reports, as did the advantage of transactions also being possible offline (they are cleared when the terminal is back online). Systems that specifically demand stable internet access do not go far in Ghana’s impoverished northern regions.

Around 40,000 people in the 60 poorest districts of the country take part in the GSOP job creation scheme, which also entitles Askia Mborta to a wage of GHS 8 (the equivalent of EUR 1.60) per day. For instance, these workers improve roads or revegetate derelict farmland. Men and women receive equal pay for equal work. “We pay small sums to many, many people in the country,” Austin says. The people would previously have waited six months for their money; today with e-zwich, they have it within four weeks. In addition, only those who earned the money are able to collect it.

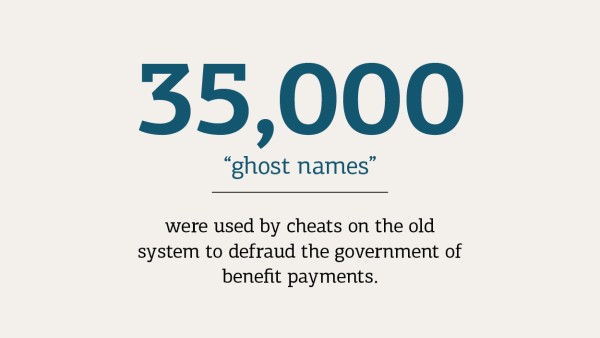

By comparing data of e-zwich cardholders with data from payrolls, the National Service Scheme (NSS) alone found 35,000 “ghost names” among its files. The NSS is a mandatory national service programme in which all Ghanaians over the age of 18 must do a year of community work, whether in agriculture, education or healthcare. For this, they receive GHS 350 (equivalent to around EUR 74) a month.

Askia Mborta is thankful that she no longer needs to make the run to the bank in the nearest town for cash.

When the NSS switched all payments over to e-zwich with biometric data, it emerged that around half of the payees were fraudsters who had simply added a second or third NSS name. After the data were purged, “the government saved GHS 12 million every month,” Archie Hesse reports. e-zwich also makes it possible to fight the widespread corruption.

In some cases, such as that of worker Askia Mborta, the bank comes to the customer with e-zwich, though naturally it can also work the other way around. Cash points with fingerprint scanners are needed to be able to use the system outside of bank opening times. Thirty-four units, each costing around EUR 24,000, have been purchased to date with the aid of KfW loans. The Rural Bank in the district capital of Wenchi has acquired four of these just for its own institution, which is seven hours’ drive north of Accra and provides 5,000 customers with the e-zwich card.

Bank director Yaw Odame explains why the biometric system is superior to the PIN process of other cash cards: “We have many customers with low levels of school education who are not too strong when dealing with numbers.” With e-zwich, however, poor people can also become account holders, as the revenues generated with the card provide indication of a customer’s creditworthiness, which is a pre-requisite for opening an account.

SOURCE

This article was published in the spring/summer 2017 issue of CHANCEN magazine focusing on “Success in the Digital World”.

To German editionAskia Mborta has been a participant in the e-zwich system for a year. The small piece of plastic is a type of digital connection to living environments that are far removed from her own. Six mornings a week, she plants acacias on the bank of the nearby river along with her fellow villagers. She receives GHS 224 a month from GSOP for this. “The money helps my four children,” she says with a smile. Thanks to the card, she does not need to make the arduous journey to town to obtain the money.

The cash card e-zwich remains in demand in Ghana.

Followed up on 7 December 2020

E-zwich remains an important tool in Ghana's cashless payment system. The Ghana Social Opportunities Project (GSOP) has been succeeded by the Ghana Productive Safety Net Project (GPSNP), which aims to help end extreme poverty and increase the productivity and income of the poor. The GPSNP is co-funded by the Ghanaian government and several international donors, and implemented jointly by the Ghanaian Ministries of Gender, Children and Social Protection, and Local Government and Rural Development. The programme has three components for poverty reduction, productive inclusion and employment promotion. All three use e-zwich for social benefits, cash grants and wage payments. Poverty reduction activities include cash transfers to extremely poor households. A unique feature here is that beneficiaries also receive free health insurance. The aim is to alleviate short-term poverty and promote long-term human capital development. Other initiatives including the Students Loan Trust Fund, Teachers Training Allowances, National Service Scheme, School Feeding Programme, Nation Builders Corps (NABCO), Youth Employment Agency and Nursing Training Allowances also use e-zwich for payments, which has lead to a significant improvement in transparency while at the same time bringing about high efficiency gains in these areas. Arndt Wierheim, Head of KfW's Ghana Office, says: "We are pleased that e-zwich, with its 3.2 million cardholders and a corresponding spread, can reach over 330,000 households in poverty reduction alone, and that the system is being used by a growing number of other initiatives. This shows that the introduction of this card was worthwhile and that e-zwich is a success."

In addition, the market has evolved with new achievements, as Pascal Saavedra-Lux, who is now KfW's portfolio manager for e-zwich, reports: "With the introduction of payment interoperability and the "gh dual card", which can be used for both e-zwich and ATM transactions, the Ghanaian government and GhIpSS, Ghana’s Interbank Payment and Settlement Systems , have managed to improve flexibility and continuity of payment flows between e-zwich wallets, mobile money wallets and bank accounts, while reducing transaction costs. A brand new biometric e-zwich POS device was also introduced to the Ghanaian market. The new hybrid device, which supports both e-zwich and ATM services, is expected to improve usage."

Isaac Hagan, KfW Financial Sector Project Coordinator in Ghana, commends e-zwich for its contribution to financial and socio-economic inclusion and development. He points out that through the partnership of KfW, the Ghanaian Ministry of Finance and GhIpSS, the e-zwich Rural Branchless Banking Project has procured 105 ATMs, 3,300 POS devices and over 1.1 million cards for use.

The described project contributes to the following United Nationsʼ Sustainable Development Goals

Goal 9: Build resilient infrastructure, promote sustainable industrialization and foster innovation

Non-existent or dilapidated infrastructure hinders economic efficiency and thus engenders poverty. When building infrastructure, the focus should be on sustainability, for example, by promoting environmentally-friendly means of transport. Factories and industrial facilities should also ensure that production is in line with ecological aspects to avoid unnecessary environmental pollution.

All United Nations member states adopted the 2030 Agenda in 2015. At its heart is a list of 17 goals for sustainable development, known as the Sustainable Development Goals (SDGs). Our world should become a place where people are able to live in peace with each other in ways that are ecologically compatible, socially just, and economically effective.

Published on KfW Stories: Monday, 12 June 2017, last updated: 7 December 2020.

Data protection principles

If you click on one of the following icons, your data will be sent to the corresponding social network.

Privacy information