Economic Outlook

Comments of KfW Research

31.07.2026 | Inflation euro area July 2026

„Fluctuations in inflation in the eurozone reflect the conflict in the Middle East. Following the collapse of the framework agreement between the US and Iran, global energy prices have risen again. Whilst oil prices are still below the highs seen since the outbreak of the war, European gas prices have returned to those levels. For European consumers, this means that prices at the petrol pumps are rising again during the holiday season. However, there is still little evidence of a significant broadening of inflationary pressure. Data from the ECB point to a stable outlook for collectively agreed wages and companies’ expectations for selling prices have fallen. We therefore expect that, apart from a second rate hike by the ECB in September, there will be no further monetary tightening.”

Stephanie Schoenwald

German Economy / European Economy

KfW Business Cycle Compass Germany / Eurozone

Iran war dampens growth prospects

27 May 2026

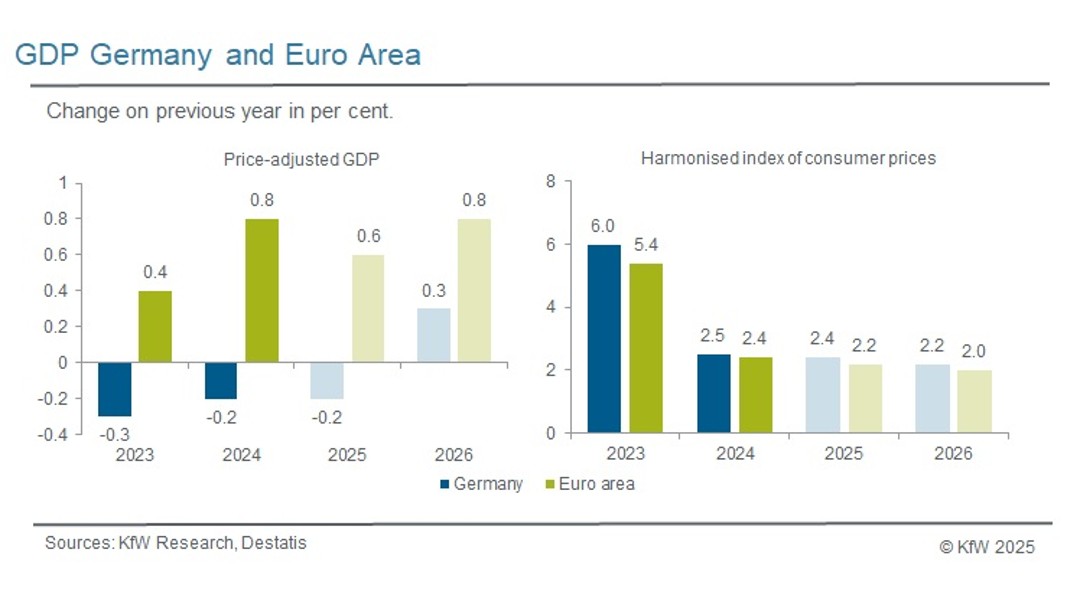

The German economy has made a solid start to the year, with growth of 0.3% quarter on quarter. However, the war in Iran is now clouding the economic outlook: KfW Research expects real gross domestic product (GDP) in Germany to increase by only 0.7% in 2026, followed by 1.3% in 2027. We have also revised our forecasts for real GDP in the euro area noticeably downwards but revised our inflation forecast in the opposite direction: In 2026, consumer price inflation in both Germany and the euro area is likely to be in the 3% range.

KfW-ifo SME Barometer

SMEs play a decisive role for the growth and prosperity of an economy. Using its unique surveys, studies and statistics, KfW Research analyses the needs of SMEs in Germany. The KfW-ifo SME Barometer indicators are based on a scale-of-enterprise evaluation of the ifo economic surveys, from which the well-known ifo business climate index is calculated, among others. Around 9,500 businesses, including around 8,000 SMES, from manufacturing, construction, wholesale, retail and services (excluding lending, insurance and state) are polled monthly regarding their economic situation.

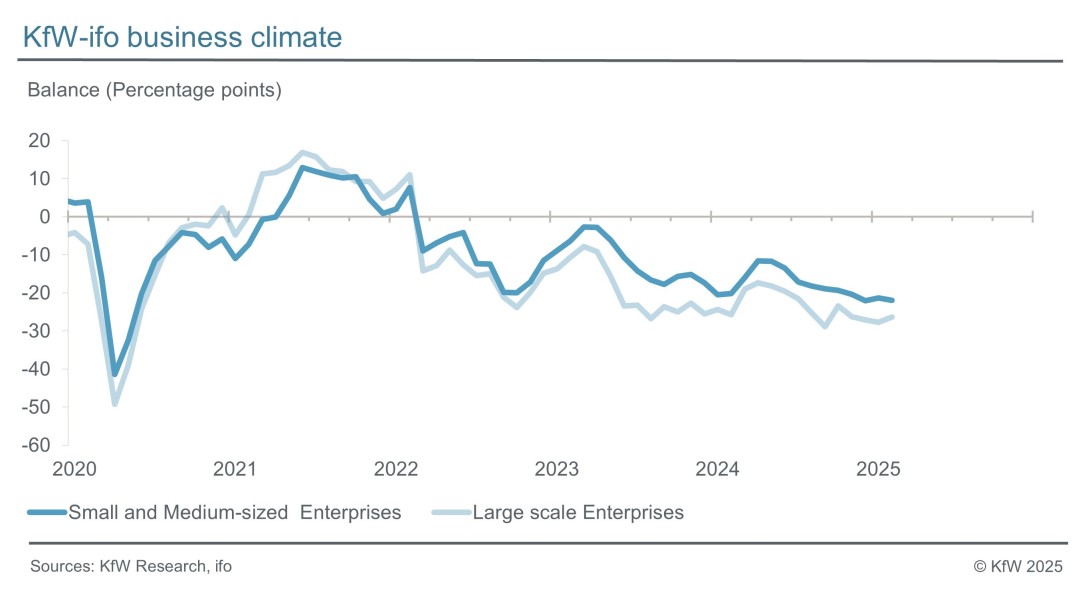

Business expectations in the SME sector surge

29 July 2026

The business climate among small and medium-sized enterprises makes a considerable leap upwards in July. It rises by 4 points to -17.3 balance points. This is mainly due to markedly improved business expectations. In all sectors of the economy, the business climate improves significantly and, in the wake of the more positive business outlook, employment expectations among SMEs have also recovered somewhat.

Contact

KfW Research, KfW Group, Palmengartenstrasse 5-9, 60325 Frankfurt, Germany,

Share page

To share the current page content with your network, click the button below and then select the desired option in the dialog box.

Note on data protection: By clicking the button, your browser's sharing function is used. If you select an external provider when sharing, personal data may be processed by the provider. Please read our data protection principles for more information.

Your browser does not support sharing with external services.

Alternatively, you can also copy the short link: https://www.kfw.de/s/enkBbw3W

Copy link Link copied